当前位置:网站首页>Understanding of expectation, variance, covariance and correlation coefficient

Understanding of expectation, variance, covariance and correlation coefficient

2022-07-08 01:23:00 【You roll, I don't roll】

Catalog

1、 Mathematical expectation ( mean value )

4、 The correlation coefficient ρ

One sentence summary : expect Reflects the average level , variance It reflects the fluctuation degree of data , covariance It reflects the correlation between two random variables ( Dimensionality ), The correlation coefficient It reflects the dimensionless correlation between two random variables .

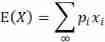

1、 Mathematical expectation ( mean value )

For random variables and their probabilities weighted mean :

![]()

The expectation here is the mean , In statistics, samples are used to replace the whole in most cases , Therefore, the average value of the sample is calculated as :

2、 variance D(X) or Var(X)

It is used to understand the deviation between the actual index and the average value , That is, it reflects the dispersion of data values .

![]()

if X Value set , Then its variance is small , conversely , X The more dispersed, the greater the variance .

D(X) Satisfy the following properties :

![]()

When X And Y Satisfy Independent homologous distribution (iid) when ,![]() , here :

, here :

![]()

there ![]() That's what we'll talk about later covariance .

That's what we'll talk about later covariance .

in addition Standard deviation ( Mean square error ) The calculation formula of is :![]() , And X Have the same dimension .

, And X Have the same dimension .

In sample analysis , The calculation formula of variance is :

Be careful : This is divided by 1/(n-1).

Why does divide appear in variance calculation n And divided by n-1 Two cases ?:

Divide n It calculates the population variance

, Divide n-1 It calculates the sample variance

( That is, the unbiased estimation of the total variance ). But in reality, it is often unrealistic to calculate the total variance , One of the research contents of statistics is to infer the population with samples , Therefore, we often use sample variance to replace the overall situation .

Why is the sample variance calculated by n-1 Well ? Because we must calculate the sample mean before calculating the sample variance

( let me put it another way , Will sum the samples ), This leads to the n If the item is determined n-1 Item's words , The first n Items can be determined , That is, the degree of freedom is n-1, So the probability of each occurrence is 1/(n-1) , So you have to divide by n-1. In terms of linear algebra , this n Quantity is not independent , If the n If a quantity is regarded as a vector, it is linearly related , Can be n-1 A linearly independent vector representation .

If divided by n It means that we know the mean value of the population sample in advance μ( This μ It is known. , Not calculated , Because in reality, it is often unrealistic to calculate the overall average ), At this time, the probability of occurrence of all quantities is 1/n, So the variance at this time

3、 covariance Cov(X,Y)

Covariance is used to describe the correlation between two variables . Covariance is a dimensional quantity .

![]()

if X And Y Are independent of each other , be ![]() .

.

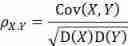

4、 The correlation coefficient ρ

The correlation coefficient is also used to describe the correlation between two variables , But unlike covariance , The correlation coefficient is a dimensionless quantity , The formula is as follows .

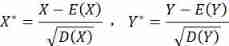

in addition , call

by X、Y Standardization of . Then there are :

![]()

The nature of the correlation coefficient :

.

. The greater the value of, the greater the degree of linear correlation , When the value is large, it is called X And Y The linear correlation is good ;

The greater the value of, the greater the degree of linear correlation , When the value is large, it is called X And Y The linear correlation is good ; Time description X And Y There is no linear relationship , But there may be other relationships , For example, for obedience

Time description X And Y There is no linear relationship , But there may be other relationships , For example, for obedience  The random variable on X Come on , if X1=sinX,X2=cosX, although

The random variable on X Come on , if X1=sinX,X2=cosX, although  , But satisfied

, But satisfied  .

. The necessary and sufficient conditions for : There is a constant a、b, bring

The necessary and sufficient conditions for : There is a constant a、b, bring

5、 Covariance matrix

Covariance matrix is used to describe the covariance between different dimensions of multidimensional random variables .

set up n Dimensional random variable ![]() The second-order covariance of is

The second-order covariance of is

![]()

Then the matrix

be called n Dimensional random variable ![]() The covariance matrix of . because

The covariance matrix of . because ![]() , Therefore, the covariance matrix is also a symmetric matrix , The variance forms the elements on its diagonal , Covariance constitutes the non diagonal element . In a general way ,n The distribution of dimensional random variables is unknown , Or it's too complicated , So difficult to deal with mathematically , Therefore, covariance matrix is very important in practical application . Covariance matrix is widely used in statistics, machine learning and other fields .

, Therefore, the covariance matrix is also a symmetric matrix , The variance forms the elements on its diagonal , Covariance constitutes the non diagonal element . In a general way ,n The distribution of dimensional random variables is unknown , Or it's too complicated , So difficult to deal with mathematically , Therefore, covariance matrix is very important in practical application . Covariance matrix is widely used in statistics, machine learning and other fields .

边栏推荐

- For the first time in China, three Tsinghua Yaoban undergraduates won the stoc best student thesis award

- 网络模型的保存与读取

- Talk about smart Park

- Basic implementation of pie chart

- Chapter improvement of clock -- multi-purpose signal modulation generation system based on ambient optical signal detection and custom signal rules

- USB type-C docking design | design USB type-C docking scheme | USB type-C docking circuit reference

- 2022 high altitude installation, maintenance and demolition examination materials and high altitude installation, maintenance and demolition operation certificate examination

- Ag7120 and ag7220 explain the driving scheme of HDMI signal extension amplifier | ag7120 and ag7220 design HDMI signal extension amplifier circuit reference

- A speed Limited large file transmission tool for every major network disk

- 2022 high voltage electrician examination skills and high voltage electrician reexamination examination

猜你喜欢

4. Strategic Learning

2022 refrigeration and air conditioning equipment operation examination questions and refrigeration and air conditioning equipment operation examination skills

Definition and classification of energy

Arm bare metal

Macro definition and multiple parameters

2021 welder (primary) examination skills and welder (primary) operation examination question bank

Recommend a document management tool Zotero | with tutorials and learning paths

Get started quickly using the local testing tool postman

2022 safety officer-a certificate free examination questions and safety officer-a certificate mock examination

跨模态语义关联对齐检索-图像文本匹配(Image-Text Matching)

随机推荐

2022 refrigeration and air conditioning equipment operation examination questions and refrigeration and air conditioning equipment operation examination skills

Blue Bridge Cup embedded (F103) -1 STM32 clock operation and led operation method

Cs5212an design display to VGA HD adapter products | display to VGA Hd 1080p adapter products

Transportation, new infrastructure and smart highway

Talk about smart Park

Chapter 5 neural network

Su embedded training - Day6

Gnuradio operation error: error thread [thread per block [12]: < block OFDM_ cyclic_ prefixer(8)>]: Buffer too small

Ag9310 same function alternative | cs5261 replaces ag9310type-c to HDMI single switch screen alternative | low BOM replaces ag9310 design

Recommend a document management tool Zotero | with tutorials and learning paths

5. Contrôle discret et contrôle continu

Introduction to the types and repair methods of chip Eco

Common configurations in rectangular coordinate system

Vs code configuration latex environment nanny level configuration tutorial (dual system)

基础篇——整合第三方技术

2022 high voltage electrician examination skills and high voltage electrician reexamination examination

4、策略学习

How to get the first and last days of a given month

Common fault analysis and Countermeasures of using MySQL in go language

HDMI to VGA acquisition HD adapter scheme | HDMI to VGA 1080p audio and video converter scheme | cs5210 scheme design explanation